RBA Lifts Cash Rate to 4.10% as Capacity Pressures Push Inflation Higher

On 17 March 2026, the Reserve Bank of Australia raised the cash rate by 25 basis points to 4.10%. The decision was passed by a majority vote of five to four, reflecting genuine uncertainty among board members about the right call.

Inflation has fallen substantially since its 2022 peak, but picked up materially in the second half of 2025. Stronger private demand, persistent capacity pressures, and rising fuel prices linked to the Middle East conflict have the Board concerned that inflation could stay above target for longer than previously anticipated. Short-term inflation expectations have already risen. The Board judged the risks are now tilted to the upside.

Key Takeaways:

-

- Cash rate increased: The RBA raised the cash rate by 25 basis points to 4.10%, citing a material pick-up in inflation in the second half of 2025 and rising capacity pressures.

- Inflation re-accelerating: While well below its 2022 peak, inflation has picked up again, with stronger private demand and capacity pressures expected to keep it above target for some time.

- Labour market still tight: Unemployment has been running a little lower than expected, underutilisation remains low, and housing prices grew strongly over the past year, though growth moderated slightly into 2026.

- Middle East risk factor: The conflict in the Middle East has pushed fuel prices higher and introduces material uncertainty around global inflation and supply, both of which the RBA is watching closely.

- Policy stance: The Board judged that inflation risks are tilted to the upside, including on expectations, and will remain data-driven, paying close attention to global conditions, domestic demand, and labour market trends.

(Source: RBA)

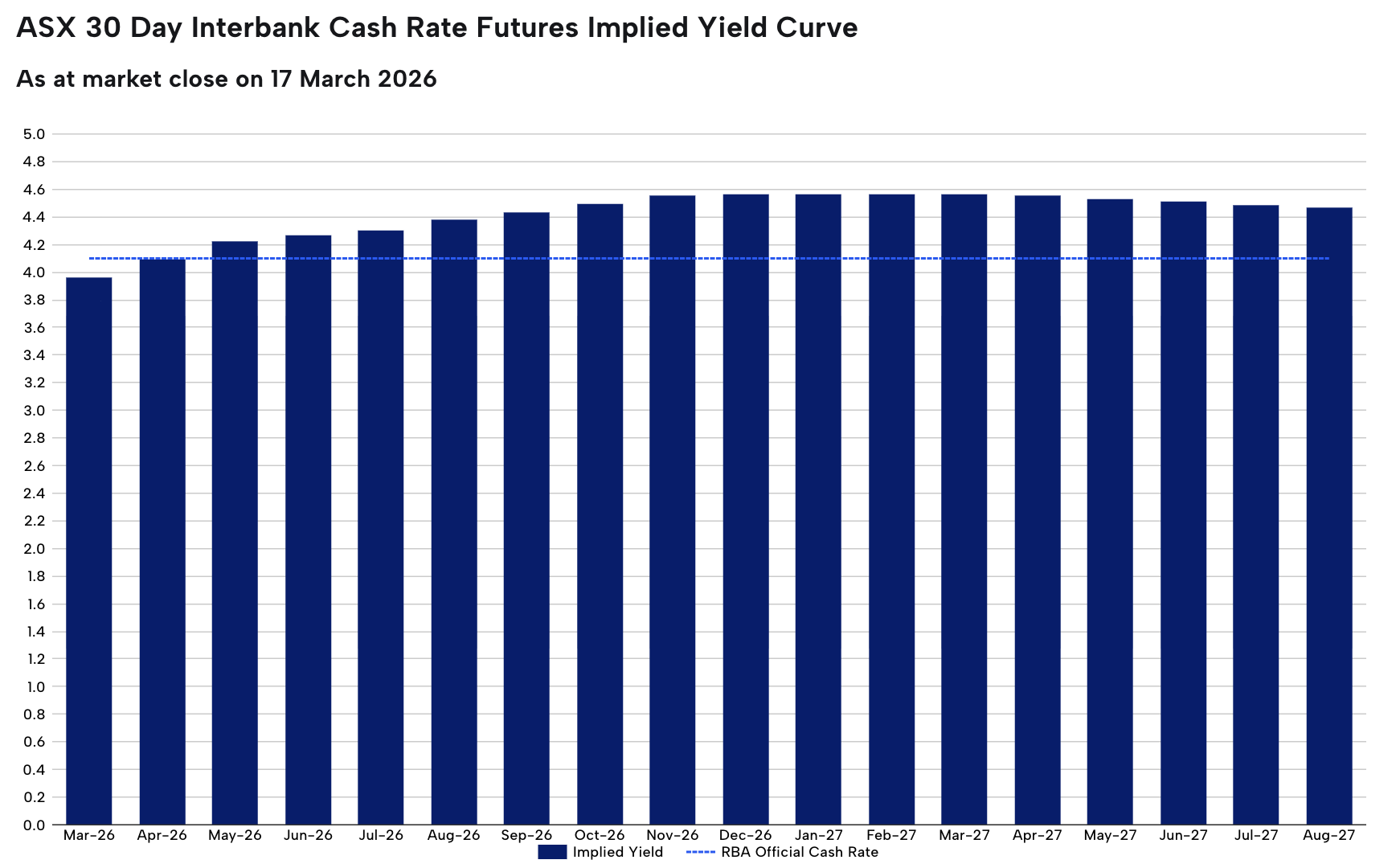

Rate Expectations

(Source: ASX RBA Rate Tracker)

On the 3rd of February the RBA increased the official cash rate by 0.25%. The current official cash rate as determined by the Reserve Bank of Australia (RBA) is 3.85%.

The next RBA Board meeting and Official Cash Rate announcement will be on the 17th March 2026.

As at the 3rd of February, the ASX 30 Day Interbank Cash Rate Futures March 2026 contract was trading at 96.14, indicating a 9% expectation of an interest rate increase to 4.10% at the next RBA Board meeting.

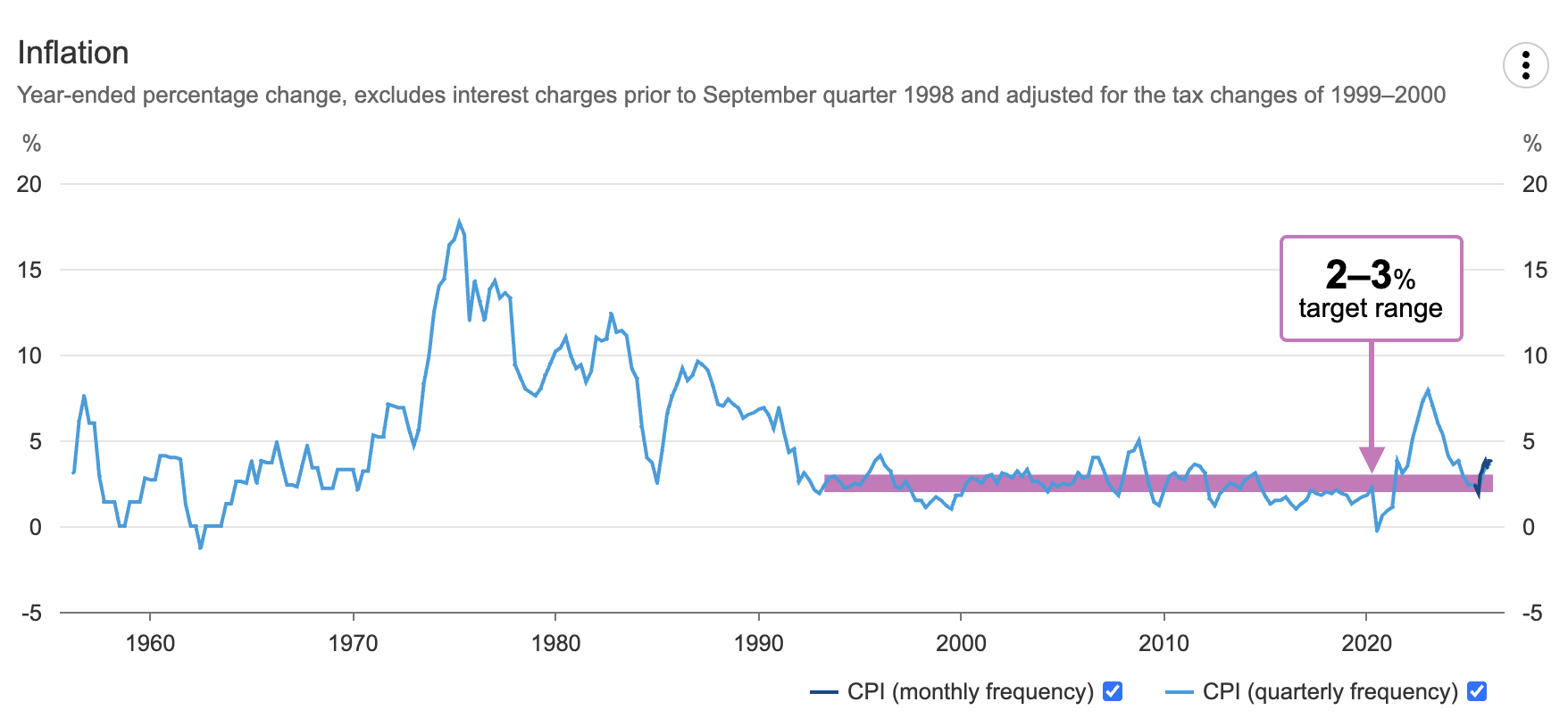

Inflation

(Source: RBA, ABS)

- Headline inflation: CPI held at 3.8% in the 12 months to January 2026, unchanged from December 2025, with housing (+6.8%), food and non-alcoholic beverages (+3.1%), and recreation and culture (+3.7%) the largest contributors to annual movement.

- Underlying inflation: Trimmed mean inflation rose to 3.4% in the year to January 2026, up from 3.3% in December 2025, sitting above the RBA’s target band and signalling that price pressures remain persistent rather than temporary.

- Household inflation (CPI): Housing remained the single largest pressure point at +6.8% annually, driven by electricity costs surging 32.2% as government energy rebates were exhausted, alongside new dwellings (+3.5%) and rents (+3.9%). Health (+3.2%) and education (+5.4%) also added to household cost pressures.

- RBA stance and outlook: With both headline and trimmed mean inflation above target, and underlying pressures building rather than easing, the Board’s decision to raise rates in March reflects a judgment that inflation is not yet on a sustainable path back to the 2 to 3% band.

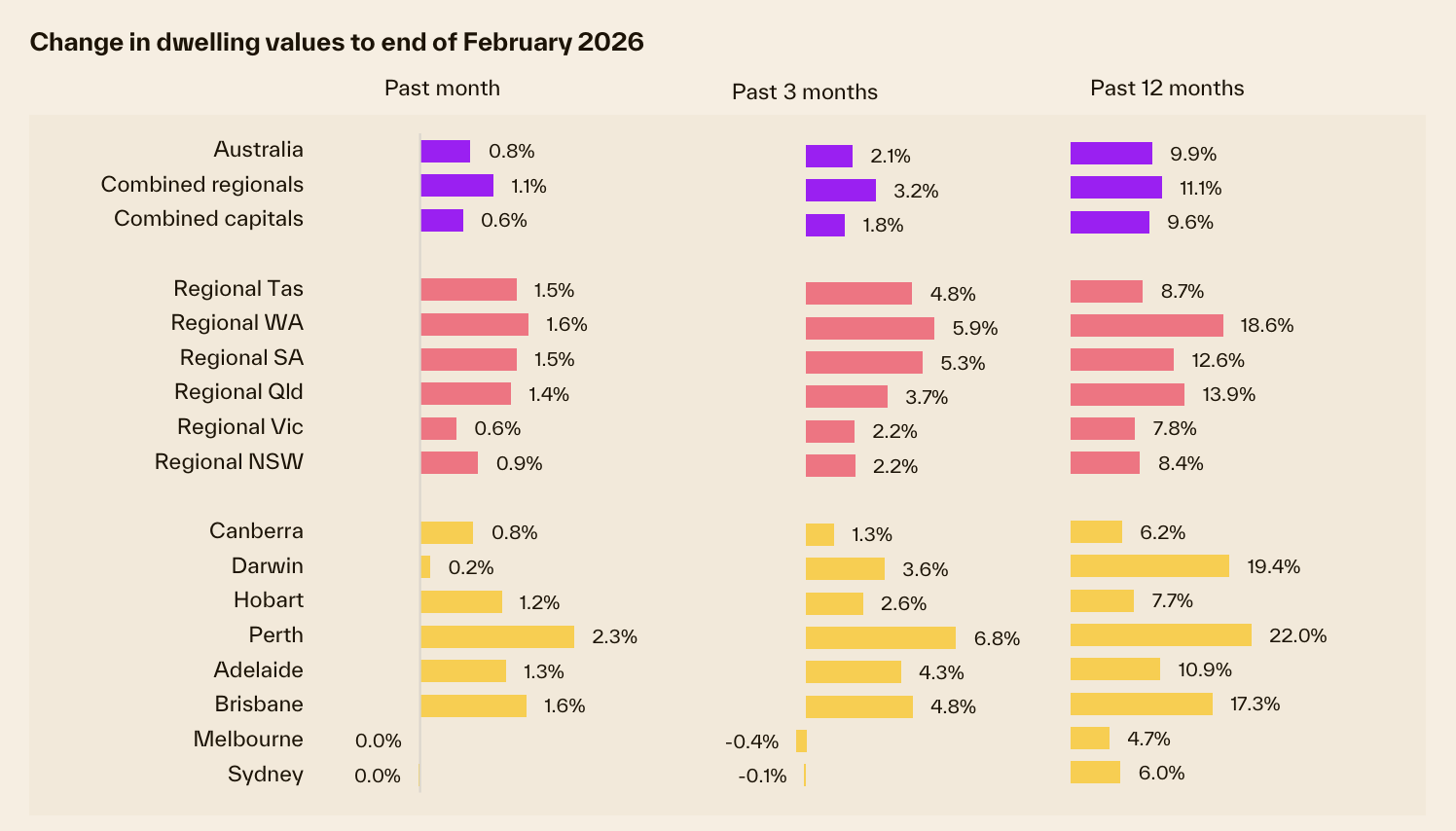

Property Market Update

(Source: Cotality March HVI)

- Home values hit record highs nationally, but the gap is widening. National dwelling values rose 9.9% annually to a median of $922,838, with Perth (+22.0%), Brisbane (+17.3%), and Darwin (+19.4%) leading the charge. Sydney and Melbourne recorded flat monthly growth (0.0% each), with Melbourne slipping -0.4% over the rolling quarter, reflecting greater sensitivity to the February rate rise and softening buyer sentiment.

- Auction and listings activity shows a market in transition. New listing flow in Sydney and Melbourne picked up sharply through February, with freshly advertised stock running 9.7% and nearly 12% above five-year averages respectively. In contrast, Perth listings remain 48% below their five-year average, Brisbane 31% below, and Adelaide 23% lower, keeping upward pressure firmly in place across those markets where supply constraints continue to support price growth.

- Regional and affordable markets are outperforming. Combined regionals rose 11.1% annually versus 9.6% for combined capitals, with demand supported by lower price points and rising internal migration. Within capital cities, the more affordable end of the market is also holding up strongest. In Sydney, lower quartile house values rose 0.8% in February, while upper quartile values fell 0.9%, a pattern consistent across most cities as serviceability constraints limit competition at higher price points.

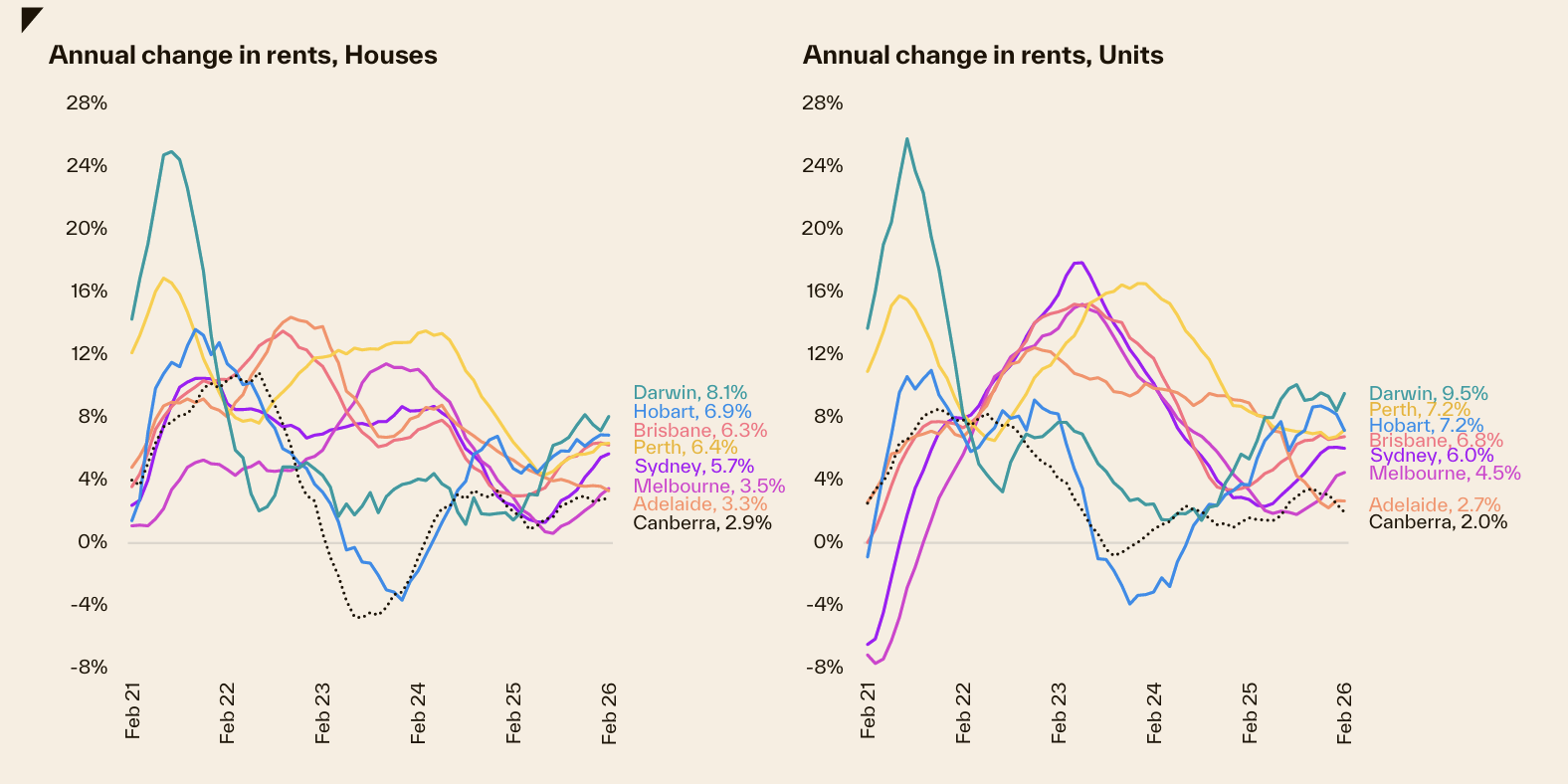

Rental Market Update

(Source: Cotality March HVI)

-

- National rental growth re-accelerating: The national rental index rose 0.7% in February, with rents up 1.7% over the rolling quarter, the strongest three-month gain since April 2025. Annual rental growth of 5.5% signals renewed pressure on tenants after a period of relative easing through much of 2025.

- Vacancy rates remain tight: National vacancy rates sit at around 1.5%, according to Cotality’s March 2026 Housing Chart Pack. While some apartment markets have seen additional supply come online, helping to moderate unit value growth, overall rental supply remains insufficient to meaningfully ease competition for tenants across most capital cities.

- Multi-speed conditions across capitals: Darwin recorded the sharpest annual rental growth at 8.6% for houses and 9.5% for units. Sydney house rents rose 5.7% annually. Adelaide eased to 3.2%, while Canberra remains the softest market at 2.9% for houses and 2.0% for units, reflecting low population growth and above-average dwelling completions.

- Yields tight, cash flow still a challenge: Gross rental yields sit at 3.4% for combined capitals and 4.2% for combined regionals. For most new investors, holding costs will likely outpace rental income unless they carry a large deposit or are buying in higher-yielding markets like Darwin or select regional locations.

The RBA increase to a 4.10% cash rate marks a definitive shift in the monetary cycle. Inflationary pressures re-accelerated in late 2025, and the Board now expects these levels to persist above the target band for longer than previously forecast.

For Azura clients, the implications are direct: higher debt-servicing costs and reduced borrowing capacity.

Now is the critical time to proactively review your lending strategy. Current market conditions demand a proactive review of your entire credit structure. Whether that involves refinancing to mitigate higher costs or restructuring to preserve cash flow, your strategy must evolve.

Our team is ready to analyse your position. Let’s optimise your financial setup today.