RBA Holds Cash Rate at 4.35% as It Assesses Inflation and Growth Risks

The Reserve Bank of Australia held the official cash rate target unchanged at 4.35% at its 16 June 2026 meeting. The decision was unanimous.

The Board acknowledged that inflation picked up materially in the second half of 2025, and that data since the start of 2026 confirms some of that lift reflected greater capacity pressures in the economy. While oil prices have eased in recent weeks, energy and most commodity prices remain higher than they were before the Middle East conflict escalated. There are signs that firms facing elevated costs are passing those increases through to customers, and short-term measures of inflation expectations remain higher than they were earlier in the year.

Financial conditions have tightened this year following three cash rate increases. Money market rates and government bond yields have risen, the exchange rate has appreciated, and consumer spending growth is slowing. The housing market has shifted, with values falling in some capital cities. The unemployment rate came in higher than expected in April, though other labour market indicators have been more resilient. Business investment growth remains strong and credit is readily available.

The Board was clear that inflation is still too high. It judged that holding the rate was appropriate while it assesses the response to previous increases and the impact of the oil supply disruption. But it retained an explicit tightening bias, stating it will increase the cash rate further if required.

Key Takeaways:

-

- Cash rate: The RBA held the cash rate target unchanged at 4.35% at its 16 June 2026 meeting.

- Inflation: Headline and underlying inflation are still running above the RBA’s 2–3% target band. The Board expects inflation to remain elevated for some time.

- Capacity pressures: The RBA said some of the recent lift in inflation reflected greater capacity pressures in the economy.

- Global risks: Oil prices have eased but remain elevated relative to pre-conflict levels. Global oil supply issues are expected to take time to resolve, keeping upward pressure on energy prices and inflation.

- Second-round effects: The Board is watching closely for cost pressures flowing through to broader goods and services prices, with early signs this is already occurring in some sectors.

- Labour market: Unemployment came in higher than expected in April, though other labour market measures have shown more resilience. The Board continues to watch domestic demand and labour market conditions closely.

- Policy stance: The Board retains a tightening bias. While it held rates at this meeting, it stated it will do what is necessary to achieve its mandate, including increasing the cash rate further if required.

- Outlook: The Board remains data-dependent, with particular attention on the path of inflation, domestic demand, and global financial conditions.

(Source: RBA)

Rate Expectations

![]()

(Source: ASX RBA Rate Tracker)

On the 16th of June the RBA left the official cash rate unchanged. The current official cash rate as determined by the Reserve Bank of Australia (RBA) is 4.35%.

The next RBA Board meeting and Official Cash Rate announcement will be on the 11th August 2026.

As at the 16th of June, the ASX 30 Day Interbank Cash Rate Futures August 2026 contract was trading at 95.61, indicating a 25% expectation of an interest rate increase to 4.60% at the next RBA Board meeting.

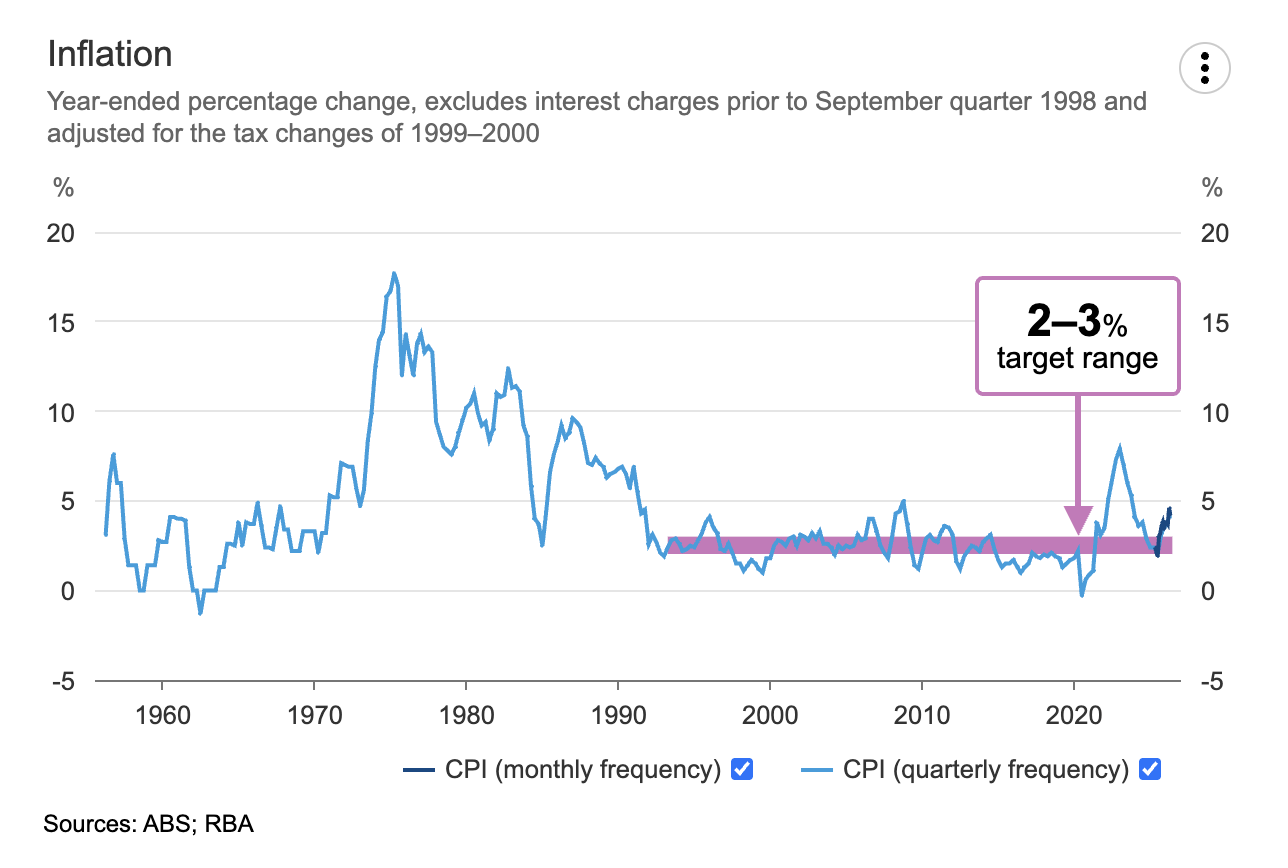

Inflation

(Source: RBA, ABS)

-

Headline Inflation: Australia’s CPI rose 4.2% in the 12 months to April 2026, down from 4.6% in the 12 months to March 2026. While headline inflation has eased, it remains above the RBA’s 2-3% target band.

-

Underlying Inflation: Trimmed mean inflation was 3.4% in the 12 months to April, up from 3.3% in March. This keeps underlying inflation above the RBA’s target band and shows that inflation pressure remains persistent.

-

Household Inflation (CPI): The largest contributors to annual inflation were Housing (+6.3%), Transport (+6.6%) and Food and non-alcoholic beverages (+2.8%). Automotive fuel was still a key pressure point, rising 18.6% over the year, although prices fell 7.0% in April after the fuel excise was reduced.

-

RBA Stance and Outlook: The RBA said inflation is still too high and that risks remain uncertain. Higher oil prices have added directly to inflation, and the Board remains focused on preventing inflation from becoming embedded.

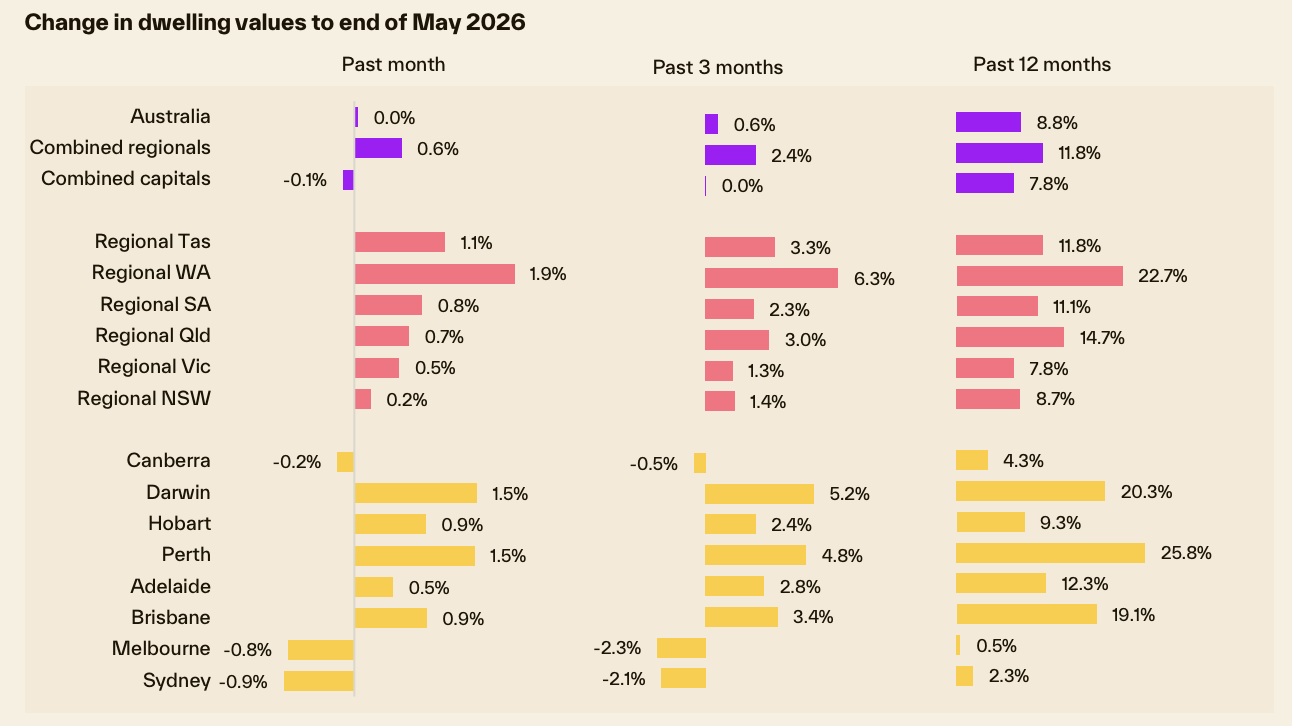

Property Market Update

(Source: Cotality June HVI)

-

National home values were flat in May, with Cotality’s national Home Value Index recording a 0.0% monthly change. Over the year, national dwelling values were up 8.8%.

-

The national result masked clear differences between markets. Perth and Darwin led the capital city gains, both rising 1.5% over the month, followed by Brisbane and Hobart at 0.9%. Adelaide rose 0.5%.

-

Sydney and Melbourne were the weakest capital city markets, falling 0.9% and 0.8% respectively in May. Canberra also recorded a fall, down 0.2% over the month.

-

Cotality noted that demand-side headwinds are intensifying. Affordability and serviceability pressures are weighing on buyer activity, estimated national home sales over the past three months were 2.2% lower than a year ago and 4.1% below the five-year average, and selling conditions have softened as supply and demand rebalance.

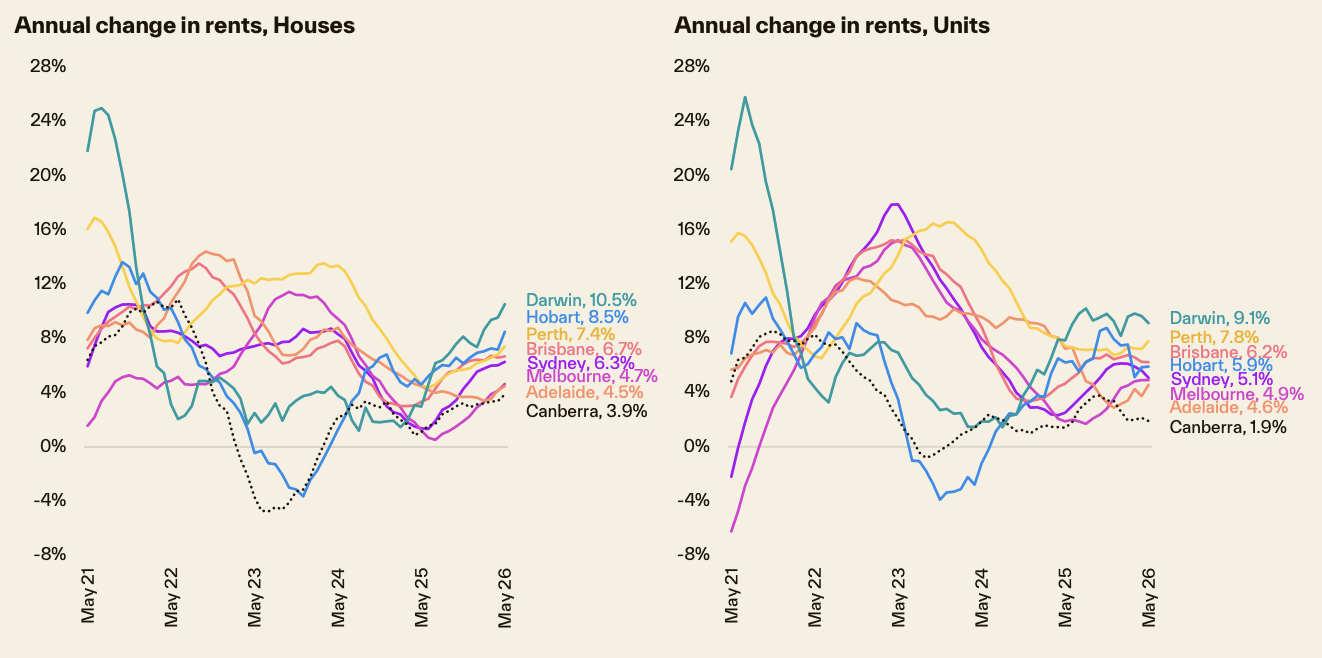

Rental Market Update

(Source: Cotality June HVI)

-

-

National rents increased 0.6% in May, matching the rise recorded in April, but easing from the 0.7% monthly gains seen through the first three months of 2026. Annual national rent growth rose to 5.9%, the largest annual increase since the 12 months ending September 2024.

-

Vacancy rates remain tight: The national vacancy rate dipped to 1.5% in May. Cotality noted this is in line with the record lows seen in 2022 and 2023, when the catch-up phase of overseas migration pushed vacancy rates lower.

-

Darwin recorded the strongest annual rental growth, with house rents up 10.5% and unit rents up 9.1% over the year. Perth was also strong, with house rents up 7.4% and unit rents up 7.8%.

-

Yields are under some upward pressure: National gross rental yields sit at 3.6%, with combined capital city yields at 3.5% and combined regional yields at 4.2%. Cotality noted that yields are rising as rents continue to increase while home value growth eases or turns negative in some markets.

What this means if you’re a borrower

For variable rate borrowers, this month’s hold means there isn’t an immediate cash rate increase flowing through from the RBA decision. That said, rates remain elevated, and household budgets are still being tested by inflation, repayment commitments and broader cost-of-living pressure.

If you’re on a fixed rate that’s due to expire soon, the key issue is still the gap between your current repayment and your likely revert rate. It’s worth reviewing this before the fixed period ends, not after, so you’ve got time to assess your options and avoid being forced into a rushed decision.

For buyers and refinancers, lender selection, loan structure and borrowing capacity remain important. Some property markets are cooling, but that doesn’t automatically mean borrowing is easier. Your position will depend on your income, expenses, deposit, existing debts, property goals and the lender policies available to you.

For investors, rising rents and firmer yields may support the numbers in some areas, but higher interest rates, holding costs and tighter serviceability settings still need careful testing. The right structure can make a meaningful difference, especially where the market is moving at different speeds across cities and price points.

This is a month to review, test and prepare. The borrowers who are best placed won’t be the ones waiting for certainty, they’ll be the ones who understand their position early and make decisions with clear advice.

Talk to the Azura team to get clear, tailored guidance on where you stand and what your options look like from here.