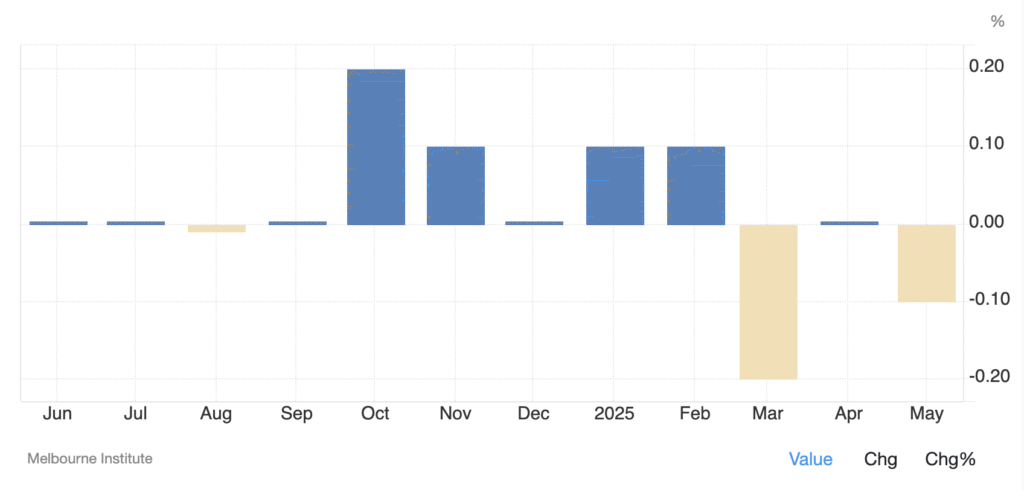

Australia’s economic recovery continues, but signs of fragility are emerging beneath the surface. The Westpac-Melbourne Institute Leading Index — a forward-looking economic indicator — edged 0.1% lower in May 2025, following a flat reading the month prior. This subtle dip suggests that the forces shaping the economy are now less global, and increasingly domestic.

Domestic Momentum Slowing

The six-month annualised growth rate of the index dropped from 0.19% to just 0.08%. According to Westpac’s Head of Macro-Forecasting, Matthew Hassan, the country’s GDP is now expected to grow at 1.7% year-on-year by the end of 2025 — a downward revision from previous forecasts and well below Australia’s long-term average growth rate.

He noted a combination of weaker global trade and shifting domestic conditions as key factors. “As government stimulus winds down, private demand is yet to fully pick up the slack,” Hassan explained. For homeowners and investors alike, this period represents a bumpy transition with pockets of opportunity and caution in equal measure.

Are These Headwinds Permanent?

Not necessarily. Some of the current drag may be transitory — including seasonality in consumer demand or temporary softness in housing starts. However, what’s clear is that Australia is now entering a more delicate phase of its economic cycle. This makes it all the more important for borrowers to assess their financial strategies, especially those considering refinancing, leveraging equity, or planning property acquisitions in 2025.

Implications for Interest Rates

Looking ahead to the RBA’s July 7–8 board meeting, economists are divided on whether they expect the Reserve Bank to keep rates on hold.

With updated economic forecasts due in August, Westpac is predicting a 25 basis point reduction, as the RBA weighs easing inflation against a slowing domestic economy.

Most analysts now agree: the peak of the rate cycle is behind us. The real question is not if rates will fall — but when, and how far. For borrowers, this marks the beginning of a more favourable lending environment, where proactive moves can lead to significant savings and improved structures.

What Should Borrowers Do Now?

- Review your current rate. Even a small shift in interest rates can translate to significant long-term savings. With conditions easing, now is the time to check if your loan is still working in your favour.

- Consider refinancing if your variable rate hasn’t been adjusted despite recent RBA movements, or restructuring your loan to better suit your current needs.

- Speak to a lending expert about securing flexible terms — particularly if you’re using structures like SMSFs, trusts, or non-bank lenders.

Azura Financial’s expert team works with a broad panel of lenders, including major banks, as well as private and non-bank options, to structure solutions that aren’t one-size-fits-all. Whether you’re looking to enter the market for the first time, safeguarding existing investments or planning your next acquisition, now is the time to act — before the market resets again.

📞 Book a consultation with our team today.

Or subscribe to our newsletter for timely updates, insights, and strategies to help you make confident property decisions.