Inflation

- The monthly consumer price index rose 5.2% annually to August 2023, UP from 4.9% in July…

- Most economists expect the RBA will wait for quarterly inflationary data and jobs figures before making a decisive decision, which pushes out a potential rate move to at least November

RBA Statement Summary – this is the first statement by the new Governor, Michelle Bullock

As you know, the RBA has left the cash rate on hold at 4.10% for the fourth month in a row. Key takeaways from their statement below:

- In light of uncertainty surrounding the economic outlook, the Board again decided to hold interest rates steady, which will provide further time to assess the impact of the increase in interest rates to date

- Inflation in Australia has passed its peak but is still too high and will remain so for some time yet

- Goods price inflation has eased further, but the prices of many services are continuing to rise and fuel prices have risen noticeably of late. Rent inflation also remains elevated. The central forecast is for CPI inflation to continue to decline and to be back within the 2–3 per cent target range in late 2025

- Growth in the Australian economy was a little stronger than expected over the first half of the year, but the economy is still experiencing a period of below-trend growth and this is expected to continue for a while

- Given that the economy and employment are forecast to grow below trend, the unemployment rate is expected to rise gradually to around 4½ per cent late next year

- The recent data are consistent with inflation returning to the 2–3 per cent target range over the forecast period and with output and employment continuing to grow

- The outlook for household consumption also remains uncertain, with many households experiencing a painful squeeze on their finances, while some are benefiting from rising housing prices, substantial savings buffers and higher interest income

- Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks

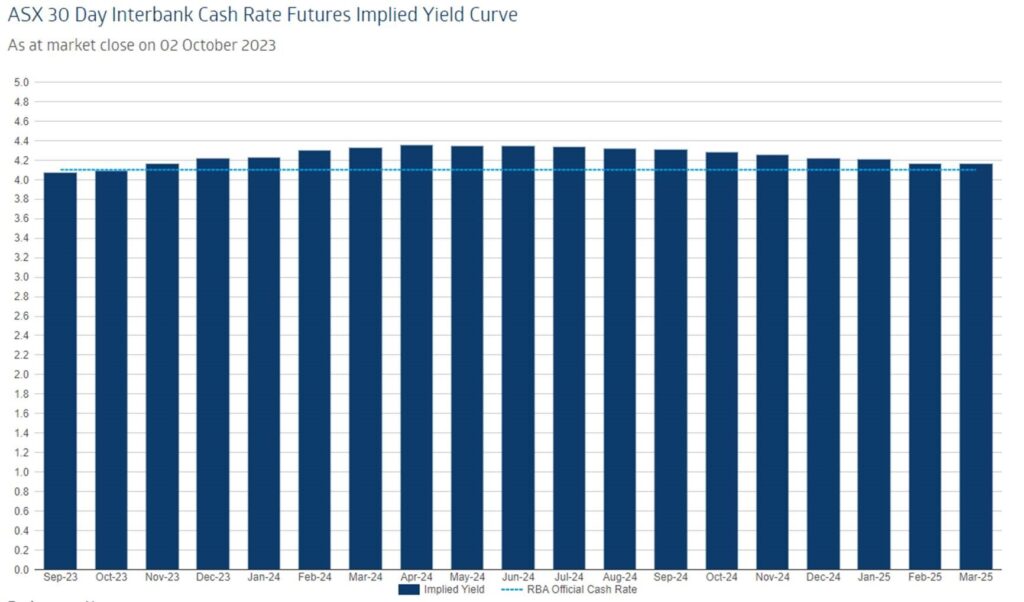

Cash Rate Expectations

After last month’s inflation print, financial markets are pricing another potential rate increase by early-mid 2024

https://www.asx.com.au/markets/trade-our-derivatives-market/futures-market/rba-rate-tracker

From Shane Oliver – Chief Economist at AMP

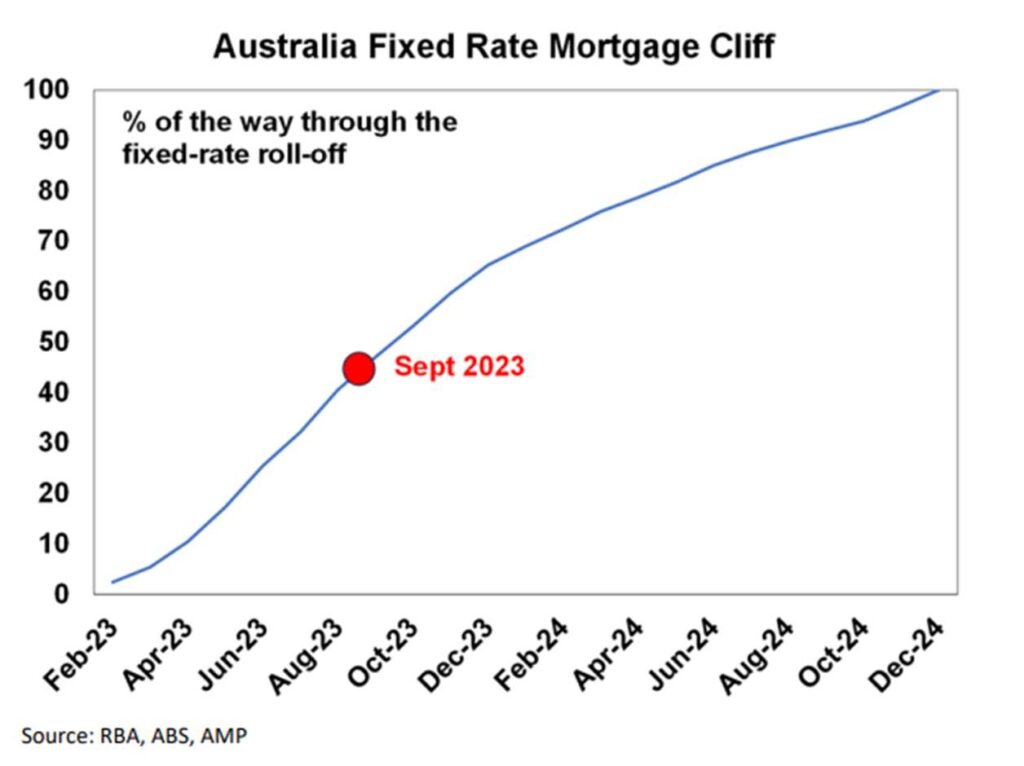

“Even though rates were left on hold, the rate hikes since May last year mean that a variable rate borrower with a $600,000 mortgage will have seen $1300 a month added to their mortgage payments. That’s an extra $15,700 a year. Even if the borrower has managed to get a 0.5% discount to their mortgage rate it would amount to an extra $13,300 which is a big ongoing hit to household spending power even if interest rates have stopped rising. Many of those on fixed rates are now starting to experience that increase now in one jump. And so far, we are only around 40% of the way through the transition from the low 2% or so fixed rates taken out through the pandemic and its immediate aftermath. The rise in mortgage rates is pushing debt servicing costs into record territory as a share of household disposable income.”

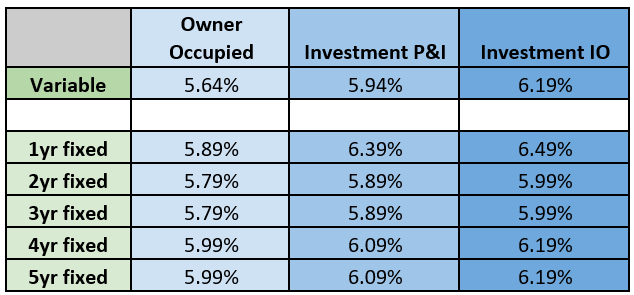

Residential Rate Card

The best mortgage interest rates we are currently seeing available for new borrowings are as follows:

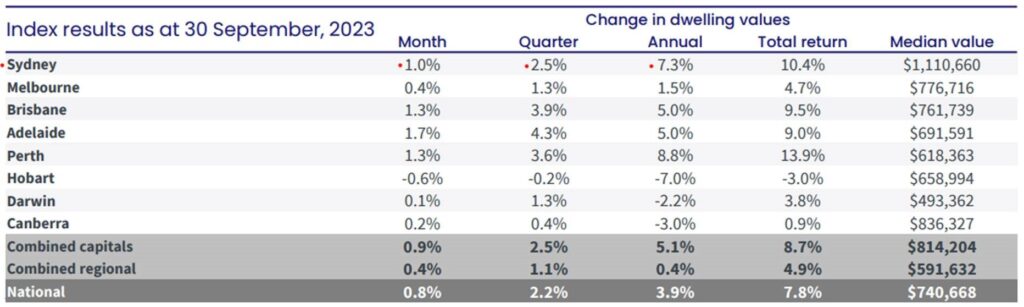

Property Market – From Core Logic – Full report here

- CoreLogic’s national Home Value Index (HVI) recorded a 0.8% rise in September as the recovery trend moved through an eighth consecutive month of growth.

- The rise follows a 0.7% lift in August (revised down from 0.8%) taking the quarterly pace of growth in national home values to 2.2%.

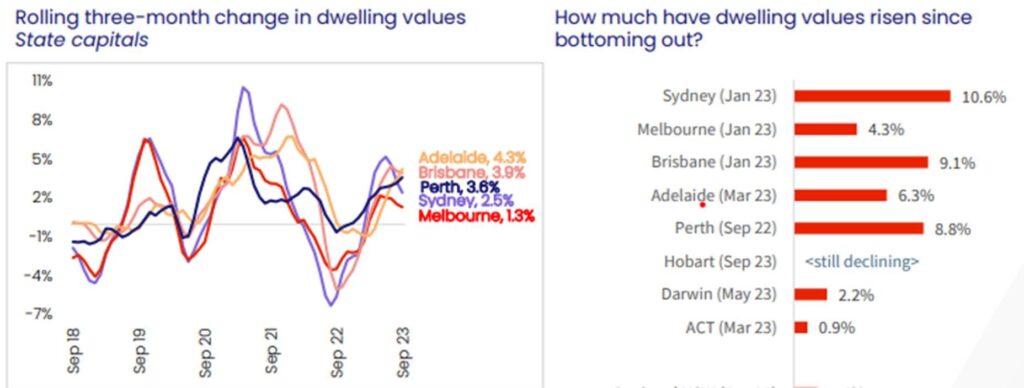

- Since finding a trough in January, the national index has recovered by 6.6%.

- Regional markets are continuing to lag the capitals with every ‘rest of state’ region recording weaker growth conditions relative to their capital city counterpart over the September quarter. At a broad level, the combined regional markets recorded a 1.1% rise in dwelling values through the September quarter which was less than half the gain across the combined capital city market (2.5%).

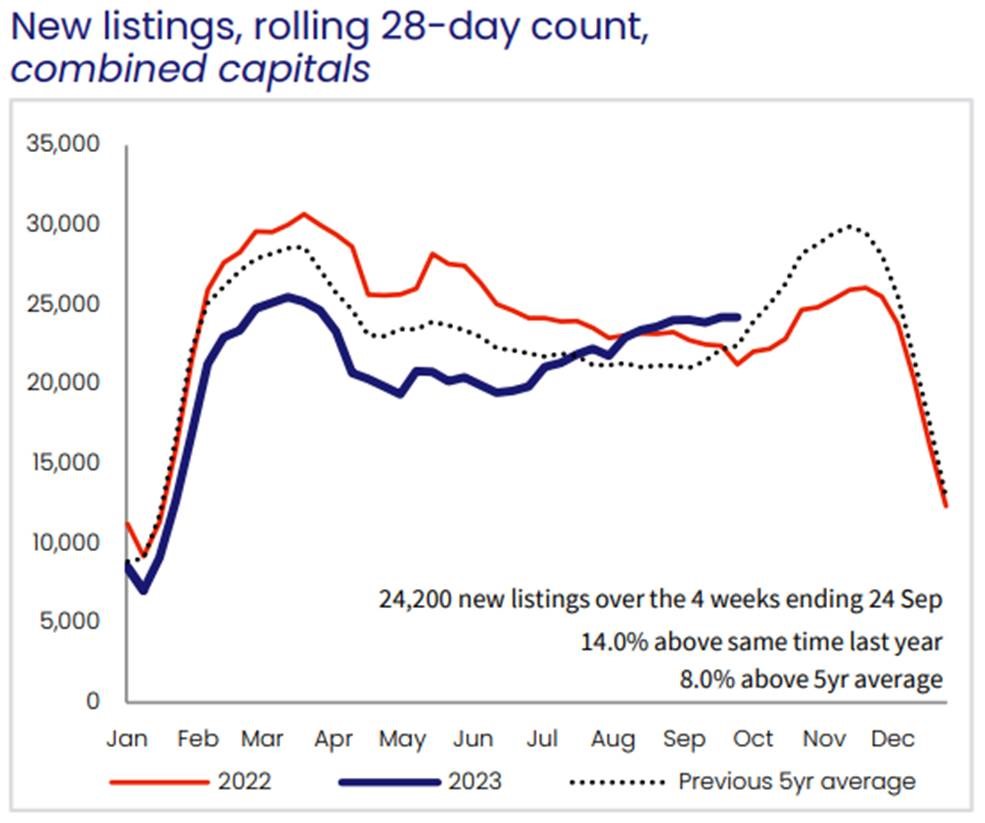

Listing Volumes – From Core Logic

- “The trend in advertised stock levels is a key influence on housing values. The flow of new listings has been on an upwards trajectory since early June, bucking the normal seasonal trend where new listings are typically flat to falling through winter. Over the four weeks ending September 24th, the flow of new capital city listings was 14% higher than at the same time last year and 8.0% above the previous five year average.”

- “Housing affordability is still relatively stretched and is getting worse as home values continue to rise. High interest rates make it harder to qualify for credit, especially when considered alongside high cost of living pressures and the three percentage point serviceability buffer. Persistently low consumer sentiment is another factor dampening housing sector activity.”